Food and beverages

Peru: A megadiverse country and a global agro-export powerhouse. Along with its rich biodiversity and varied climates, Peru offers a favorable investment environment and a resilient economy.

FDI in food and beverages

Period: 2003 - April 2024

USD

Millions of FDI in the sector.

Photo: Shutterstock

Source: fDi Markets (2024)

Projects in total.

Photo: Shutterstock

Source: fDi Markets (2024)

Jobs generated

Photo: Shutterstock

Source: fDi Markets (2024)

Potentials in food and beverages

-

Lima

-

Lima

-

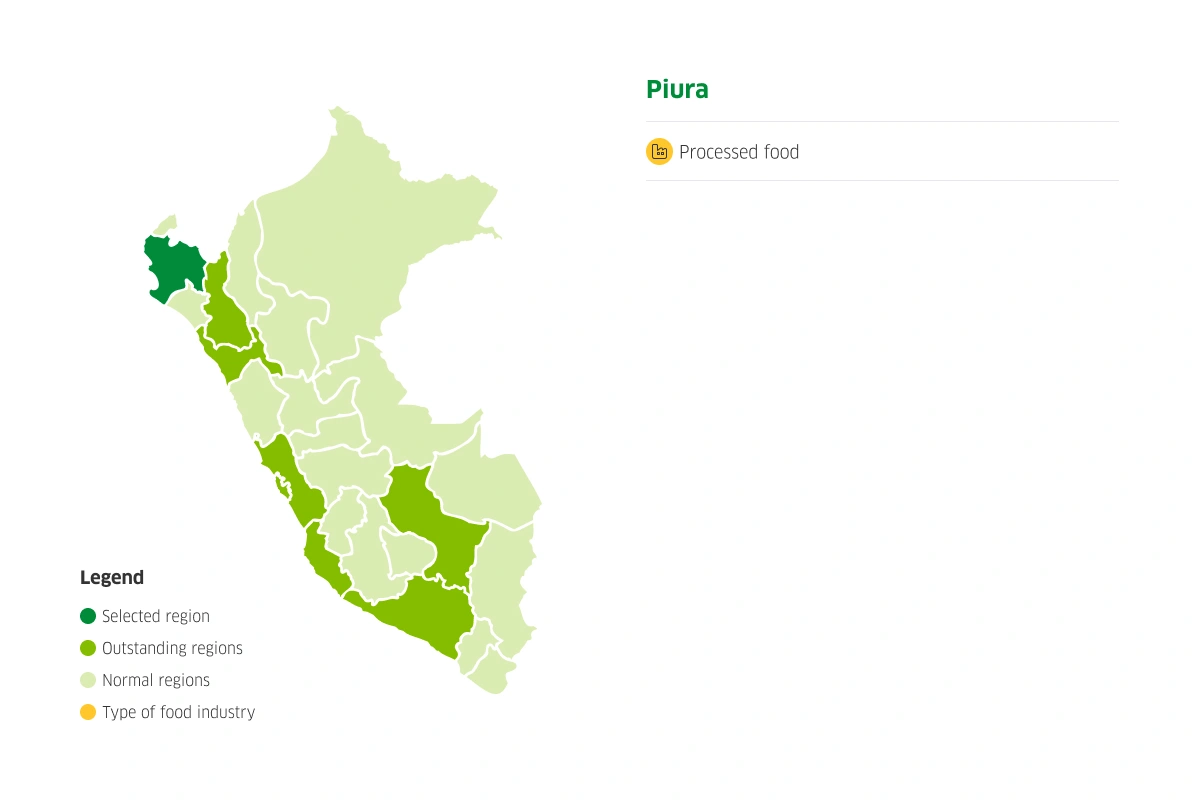

Piura

-

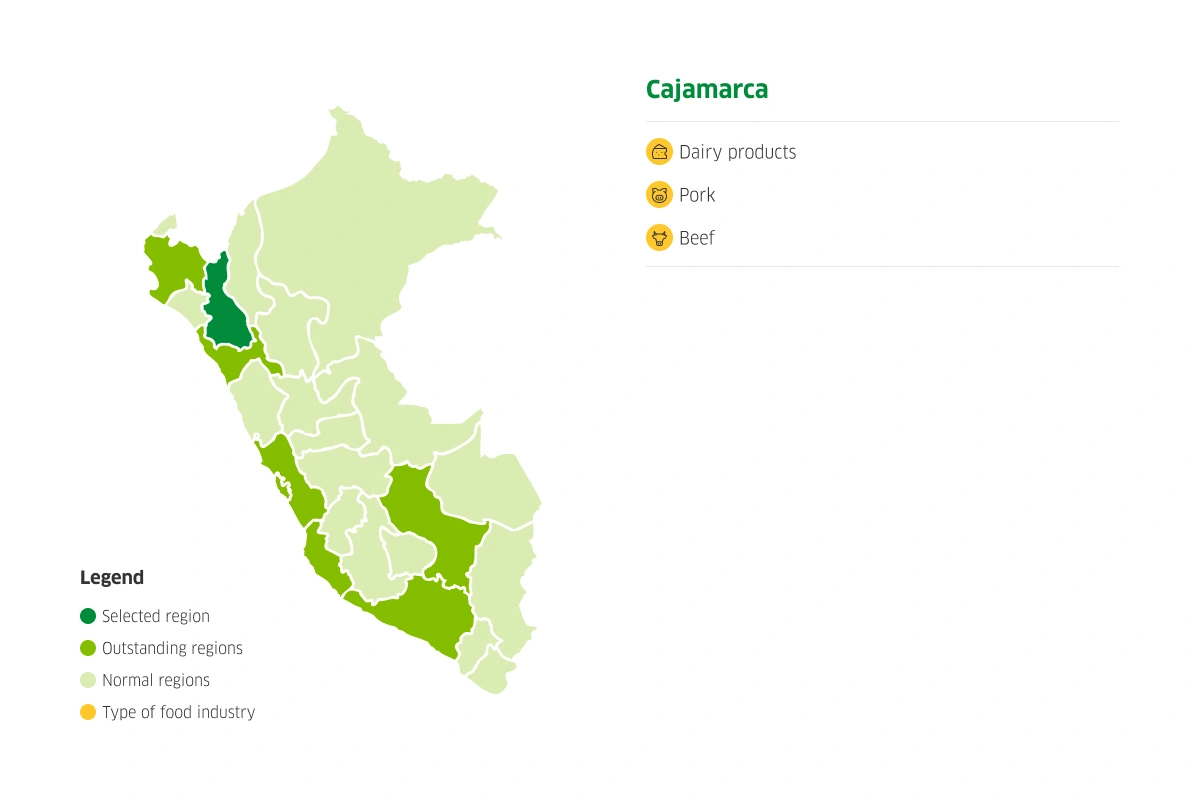

Cajamarca

-

La Libertad

-

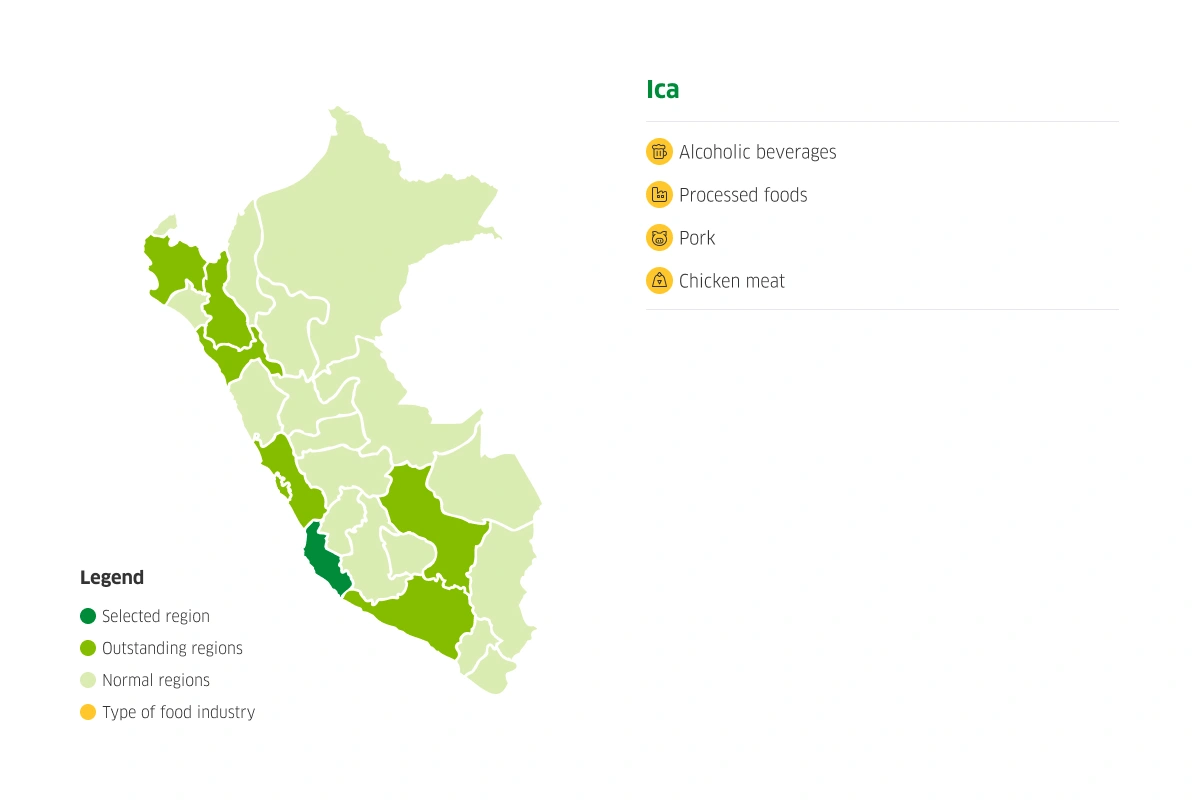

Ica

-

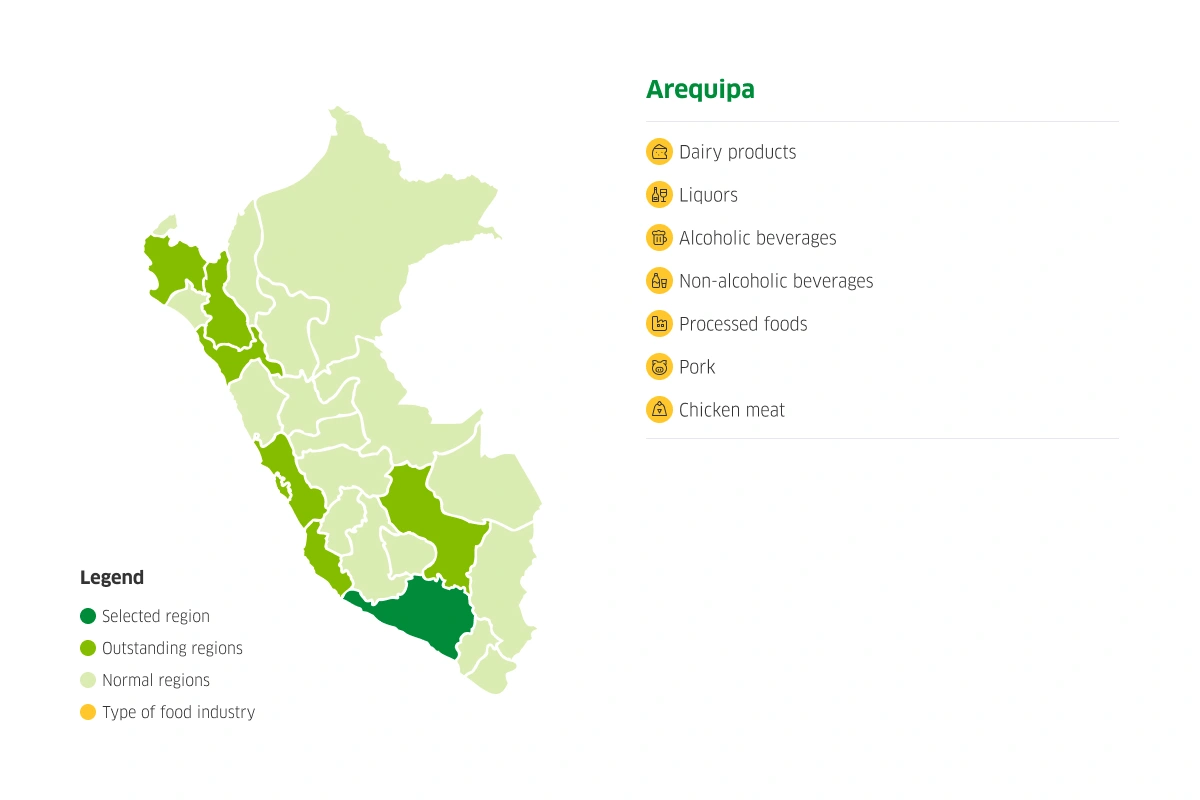

Arequipa

-

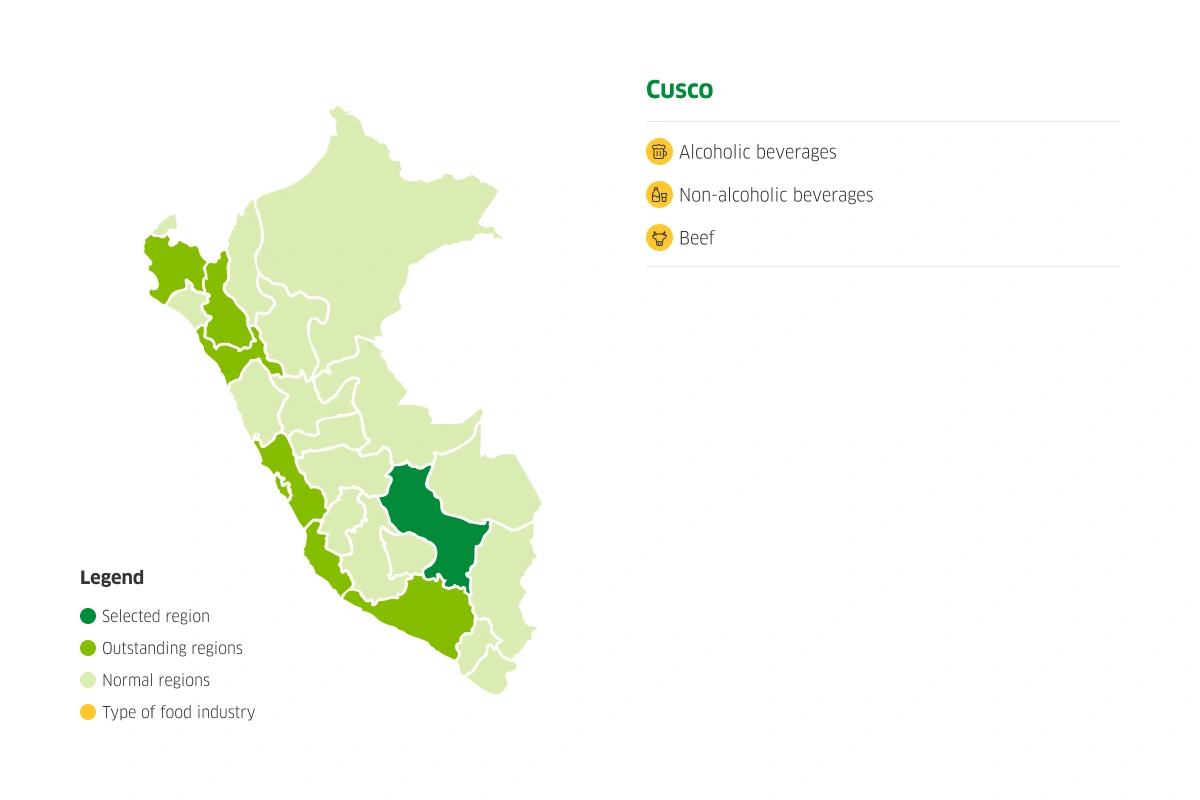

Cusco

Sector highlights

USD million of sector GDP in 2022. Average growth rate in 2016-2022 of 2 %.

Source: PROMPERÚ (2023)

In 2022, an estimated 1,000 jobs were created, with over 70 % of those held by people under 45 years old. Additionally, the number of companies is expected to exceed 34,000.

Source: PROMPERÚ (2023)

Based on expected production in 2022, Peru is ranked as the top producer and exporter of fishmeal in the world.

Source: IndexMundi (2022)

Subsectors of interest

Food and beverages

- Industrial Lines:

Processing and preservation of meat; fish, crustaceans and mollusks; and fruits and vegetables.

Processing of vegetable and animal oils and fats; dairy products; milling products, starches and starch derivatives; other food products; prepared animal foods; and beverages.

- 2022: This sector reached a historical peak, using 79.3 % of its production capacity.

Source: “Coyuntura Industrial (September 2023)”. National Society of Industries.

- 2022: The production in the beverage subsector grew by 10.2% compared to 2021

Source: “Coyuntura Industrial (February 2022 - April 2023)”. National Society of Industries.

- At the LATAM level, Peru has the most competitive industrial service costs, ranking 2nd with the lowest rates for electricity, water, and natural gas.

- Between 2018 and 2022, agro-exports recorded an average annual growth of 10.2 %.

Source: Infotrade (November 2023).

Fishing

- Capture fisheries: In 2021, Peru was the 3rd highest producer globally, with 6.5 million tons, accounting for 7.1% of the world's capture fisheries and leading in America with 37% of the region's production.

The anchoveta catch, destined for industrial consumption (19.7%) generated growth of 2.8% in the Fisheries sector in 2021.

- Fishmeal: Peru was the top producer of fishmeal in 2022.

- Direct human consumption (DCH): In 2022, of the total fish exports for direct human consumption, valued at USD 1,432.8 million, 90.4 % were frozen, totaling USD 1,390.0 million. The primary destination markets were the United States and China.

- Indirect human consumption (IHC): By 2022, China was the leading destination for Peru's fishmeal and crude oil exports.

- Biological diversity: The Peruvian coastline extends 3,080 km and reaches 200 nautical miles offshore, with access to over 1,000 fish species that have potential for direct human consumption.

Tax incentives

Anticipated recovery of the General Sales Tax (RERA IGV). D.L. No. 973 and D.L. No. 1423.

It allows projects with long pre-operational periods to recover the IGV on investments in goods, services, construction contracts, and other expenses. This facilitates company liquidity and improves its financial structure.

Law No. 31661: Provides temporary flexibility regarding the amount of investment required to benefit from this regime.

Law No. 31110: The Agrarian Labor Regime and Incentives Law for the Agrarian, Irrigation, Agro-export, and Agro-industrial Sectors.

Applicable to:

- Natural or legal persons engaged in crop cultivation and/or livestock breeding.

- Natural or legal persons involved in agro-industrial activities related to crops and/or livestock, provided these activities take place outside the province of Lima and the Constitutional Province of Callao. The law does not apply to agro-industrial activities involving wheat, tobacco, oilseeds, oils, and beer.

- Agricultural producers, excluding those organized in producer associations, as long as each individual producer does not exceed 5 hectares of production.

Income tax will have a special treatment, according to:

- Net Income up to 1,700 UIT: Taxable Years 2021-2030 (15 %) / 2031 onwards (General Regime).

- Net Income over 1,700 UIT: Taxable Years 2023-2024 (20 %) / Taxable Years 2025-2027 (25 %) / 2028 onwards (General Regime).

Depreciation

Agricultural companies are allowed to depreciate 20% per year on investments in hydraulic infrastructure and irrigation works.

Tax credit

Companies with income not exceeding 1,700 UIT are entitled to a tax credit of 10 % on the reinvestment of up to 70 % of their profits.

Law No. 27037: Law for the Promotion of Investment in the Amazon Region.

Income tax exemption:

- Income tax exemption for certain Amazonian producers.

- Taxpayers in the Amazon region who primarily engage in agricultural activities and/or the transformation or processing of products classified as native and/or alternative crops are exempt from income tax.

- The following products are considered native and/or alternative crops: yucca, soybean, arracacha, uncucha, urena, palm heart, palmito, pijuayo palmito, pijuayo, aguaje, anona, caimito, carambola, cocona, guanábano, guayabo, marañón, pomarosa, taperibá, tangerine, grapefruit, zapote, camu camu, uña de gato, achiote, rubber, pineapple, sesame, chestnut, jute and barbasco. Pursuant to Article 1 of Supreme Decree No. 074-2000-EF, published on 07/21/2000, rough cotton, curcuma, guarana, macadamia and pepper are included in the list of products qualified as native and/or alternative crops, as referred to in this paragraph.

Law No. 31666: Law for the Promotion and Strengthening of Aquaculture.

Applicable to natural or legal persons with administrative rights and current sanitary authorization to conduct aquaculture activities, in the following productive categories: Aquaculture of Limited Resources (AREL), Aquaculture of Micro and Small Enterprises (AMYPE) and Aquaculture of Medium and Large Enterprises (AMYGE), at national level, which must comply with all their corresponding tax and sanitary obligations.

The law also applies to those who carry out industrial processing (freezing, canning or curing process) for preservation and commercialization purposes.

A 15 % income tax rate applies until the year 2032 for individuals or entities whose annual income is less than 1,700 UIT. For income exceeding 1,700 UIT, the tax rate ranges from 15 % to 25 % during the same period.

For income tax purposes, agents involved in aquaculture activities can apply an annual depreciation rate of 20% on investments in aquaculture infrastructure and related equipment until December 31, 2031.

Early recovery of VAT is available on capital goods, inputs, services, and contracts incurred during the pre-operational stage of aquaculture activities.

Tax reimbursement is available for the general sales tax on acquisitions and imports of goods and inputs incurred during the preoperative stage of aquaculture activities.

Have you already invested in Peru?

We provide personalized assistance to help streamline and accelerate your investment process in Peru.